Thriv Blog

Best Freelance Marketplaces in 2026: Market, Growth, Fees, and What Users Actually Get

How the freelance marketplace category looks in 2026: market growth, platform scale, fee logic, and what clients and experts actually get on a simple $100 project.

S.N.Prakash | April 8, 2026 | 9 min

The freelance platform market is growing fast, but growth on its own does not tell you much. What matters more in 2026 is how platforms grow, how they monetize, and what clients and experts actually experience once fees, screening, and platform logic enter the picture.

One third-party market estimate from Grand View Research values the freelance platforms market at $6.37 billion in 2025 and projects it could reach $24.16 billion by 2033, implying an 18.6% CAGR from 2026 to 2033. That is still an estimate rather than a universal market fact, but directionally it fits what the category looks like: more digital work, more platformized matching, and more attention on platform economics.

The public benchmarks are still the leaders. Upwork reported $787.8 million in 2025 revenue and 785,000 active clients at year-end. Fiverr reported $430.9 million in 2025 revenue and 3.1 million annual active buyers at year-end. Those numbers matter because they show both scale and monetization, not just traffic, and both companies are publicly listed.

The right way to read this market in 2026 is simple.

How to Read This Market in 2026

- who has scale

- how platforms make money

- what that means for clients and experts

- what is changing in the category

Quick note: the public figures below are a market snapshot for clients and experts, not a strict one-to-one ranking. Some platforms publish active clients, some publish active buyers, some publish registered users, and some publish community or project-owner counts.

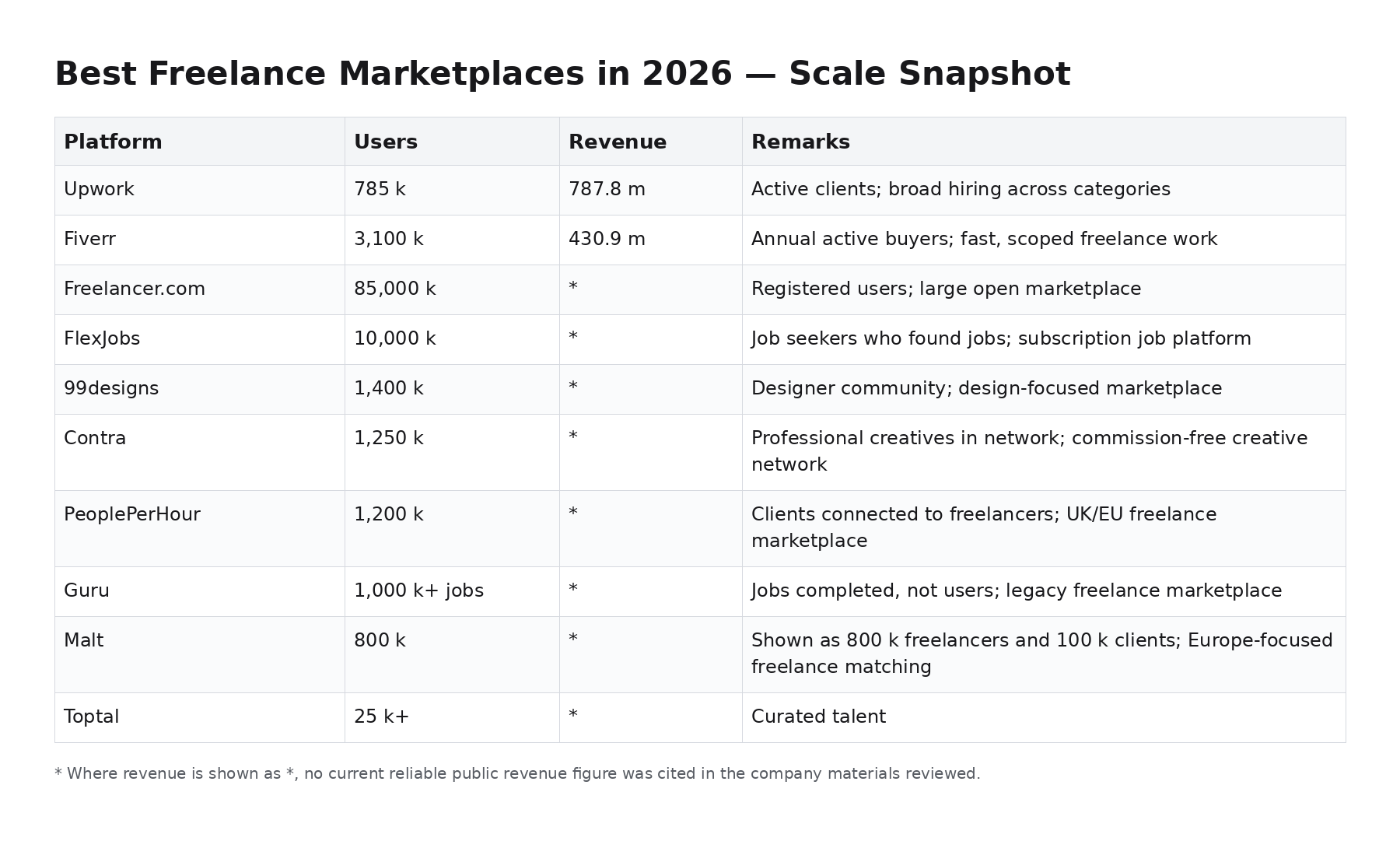

Who Has Scale

At the broadest level, Upwork and Fiverr still set the public benchmark because they give you both sides of the picture: scale and revenue. Freelancer.com also remains large on published user count. Beyond that, the market starts splitting into specialist and model-specific plays: 99designs for design, Toptal for screened premium talent, Malt for Europe-focused matching, Contra for creator-first and commission-light positioning, and FlexJobs for paid-access remote job discovery rather than a classic transaction marketplace.

That distinction matters because clients and experts do not use these platforms for the same reason. A client looking for reach and speed cares about accessible supply and transaction flow. An expert cares more about fee drag, buyer quality, repeat work, and how much of the final project value actually stays with them.

So the useful question is not which platform has the biggest number. It is which published scale signal matters for the decision you are making.

In the rest of this piece, I use clients as the simple reader-facing term for the demand side and experts as the simple reader-facing term for the supply side. The published company metrics themselves stay unchanged.

What the Scale Snapshot Actually Says

Briefly, the image above says three things. First, Upwork and Fiverr still define the public benchmark because they disclose both revenue and active client or buyer scale. Second, a large registered-user number does not automatically mean better outcomes for clients or experts. Third, several important platforms now compete on model rather than raw size: screened access, category depth, or lighter transaction fees.

Which Platforms Look Strong in 2026

If you are a client hiring across multiple categories, the broad-market names still matter most: Upwork, Fiverr, Freelancer.com, and PeoplePerHour. They are the most obvious places to start when reach and speed matter more than category purity.

If you are a client paying up to reduce selection risk, the conversation changes. Toptal and Malt stand out because they are not trying to win on the same open-market logic. They are selling screening, trust, and tighter matching.

If you are buying highly specific design work, 99designs still matters because the workflow is narrower and the market is built around that narrowness. If you are an expert or creative who cares about cleaner take-home economics, Contra matters because it does not follow the standard percentage-take marketplace model.

That is the better frame for 2026. Not one universal ranking. Different platforms are strong for different reasons, and clients and experts feel those differences quickly once money starts moving.

How They Make Money

This is where the category starts to separate. Upwork charges marketplace fees on the client side and a service fee on the freelancer side. Fiverr charges a buyer-side service fee and uses a marketplace model that still produces a high take rate. Freelancer.com, Guru, PeoplePerHour, Malt, and 99designs all take their cut differently, but the pattern is familiar: the platform earns because it sits in the middle of the transaction.

Contra is different. Its public pricing is not built around the standard percentage commission logic. It uses a lower fixed-fee structure tied to payment size, and its paid plans reduce or remove that platform fee further. FlexJobs is different in another way: it is not really a project-fee marketplace at all. It charges job seekers for access and positioning within a screened remote-work listing environment.

Once you look at the fee model closely, the category stops looking like one market. It becomes several different business models competing under the same broad freelance umbrella.

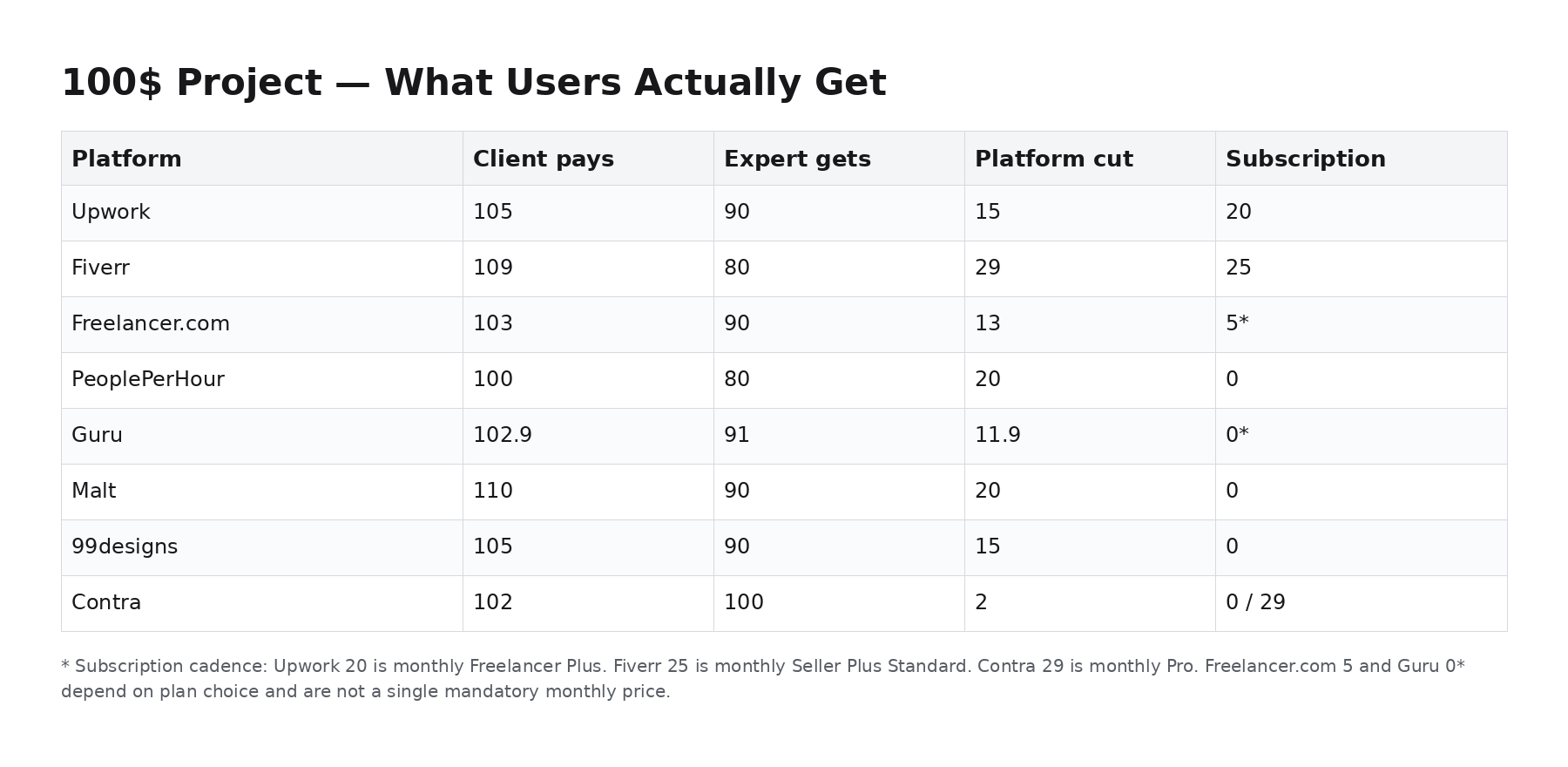

$100 Project: What Users Actually Get

The simple way to make the economics visible is to strip the marketing language away and run a small-project snapshot. A $100 project is not a perfect universal case, but it is good enough to show how quickly the client payment, expert payout, and platform cut move apart.

What the $100 Snapshot Says

Briefly, small-project math is where platform economics become visible. For clients, some platforms still feel simple because the fee is low or hidden inside the flow. For experts, the same project can look very different. If a $100 job turns into $80 net, experts either raise prices, reduce revision room, or avoid that job type entirely. That is not theory. It is the direct consequence of fee structure.

What This Means for Clients

For clients, large marketplaces still help because they reduce search cost and increase speed. You can usually get to a shortlist faster on Upwork, Fiverr, Freelancer.com, or PeoplePerHour than through slower relationship-led channels.

The tradeoff is that large supply also brings screening work, more noise, and a bigger gap between what the client pays and what the expert receives. That matters because fee drag changes behavior. When the economics get tight, experts price defensively, become less tolerant of open-ended scope, or reserve their best effort for larger or repeat engagements.

So the client-side question is no longer only, where can I find someone fast? It is also, what kind of working behavior is this fee model encouraging?

What This Means for Experts

For experts, the platform model changes incentives immediately. The sharper the cut on small work, the more likely experts are to raise minimums, avoid low-ticket projects, or move premium work off the platform where possible.

That is why Fiverr and PeoplePerHour make the economics visible so quickly on smaller jobs, while Contra stands out for creators who care about cleaner payout logic. It is also why screening-led models can still justify themselves for many experts: if the platform brings better clients and better scope discipline, a smaller volume of stronger work can beat high-volume low-margin transactions.

Experts do not only evaluate platform traffic. They evaluate what stays in their account after the platform is done taking its share.

What Is Changing in the Space

The market is maturing. Pure scale is no longer the whole story. The more interesting shift is that large platforms are pushing monetization harder, screening-led platforms are selling trust and screening, specialist platforms are going deeper by category, and commission-light models are trying to simplify the economics.

That is why clients are looking more closely at what they actually pay, what experts actually keep, and whether the platform behaves more like a connector or more like a toll gate. The category is still growing, but the debate has become more precise.

Where Thriv Fits

Most of this market is still optimized around transaction fees, service fees, or managed intermediation. Thriv is trying to position itself differently: a subscription-led, zero-commission model built around direct access, direct client-expert relationships, and clearer economics on both sides.

That matters because fee structure changes behavior. If the platform is not taking a cut from every transaction, more of the project value can stay with the expert and the client avoids the same two-sided fee distortion seen on many marketplace models. The claim is not that intermediation disappears. The claim is that the platform can make money without taxing every project in the same way.

Final Take

The freelance platform market is growing, but the real divide in 2026 is not just size. It is what kind of scale a platform has, how it monetizes, and what that does to both clients and experts.

If you want broad reach, the large marketplaces still matter. If you want screening-led matching, Toptal and Malt matter. If you want design specialization, 99designs still matters. If you want cleaner creator-side economics, Contra matters. If you want a model built around subscription and zero commission rather than project take-rates, that is the lane Thriv is trying to build.

The useful way to compare platforms now is not to ask which one is biggest. It is to ask what the platform is optimizing for, who that helps, and what gets lost in the middle.

That is the real marketplace question in 2026.

Sources

- Grand View Research: Freelance Platforms Market Size | Industry Report, 2033

- Upwork Investor Relations: News Releases

- Upwork Investor Relations: Quarterly Results

- Fiverr Investor Relations: Fourth Quarter and Full Year 2025 Results

- Freelancer Investor Page

- Contra Pricing

- Contra Fees Overview

- PeoplePerHour About

- PeoplePerHour Freelancer Commission Fees

- Malt Pricing

- Malt service offers and fees

- Guru Pricing for Employers

- Guru Pricing for Freelancers

- Freelancer.com fees and charges

- FlexJobs About

- FlexJobs Pricing

- Toptal / YouTeam page citing client trust since 2010

- 99designs: What fees do you charge for 1-to-1 Projects?

- 99designs: What is a platform fee?